Can You Use a Driver’s License at a Bank?

Visiting a Bank Without a Resident Registration Card

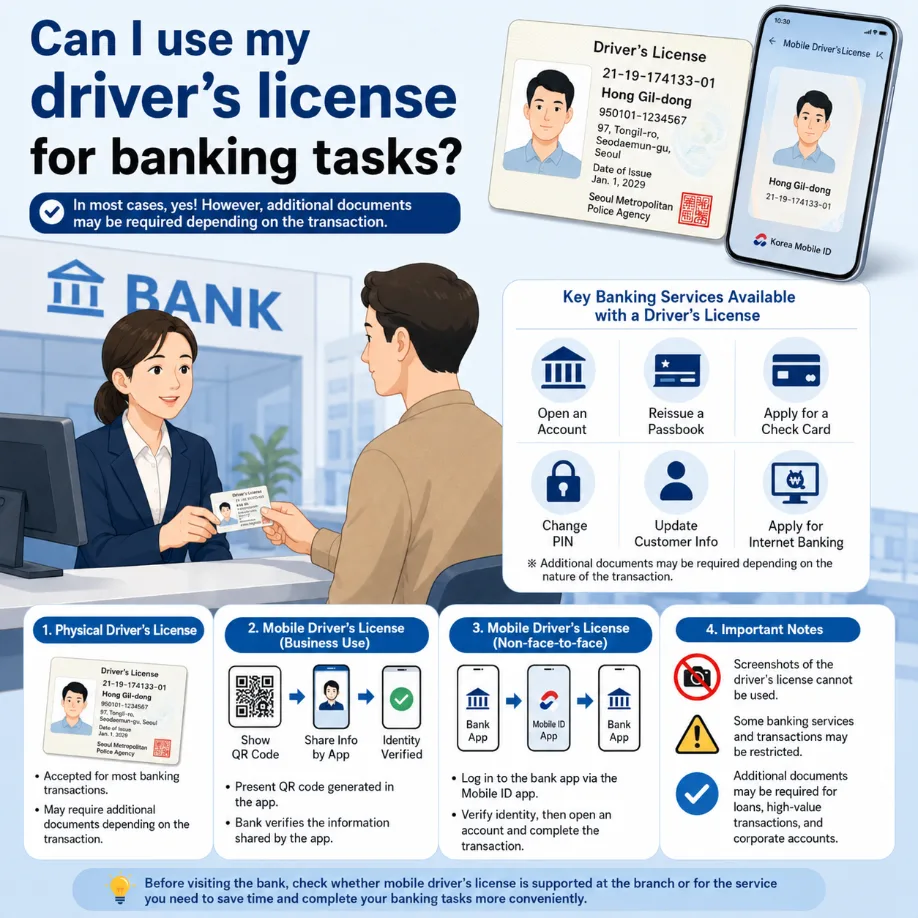

Even if you do not have your resident registration card, you can handle most banking transactions by presenting a valid driver’s license. A driver’s license contains the holder’s name, photograph, resident registration number, and other information required for identity verification, so it is generally accepted as an official identification document.

Banking Services Available at a Branch

A physical driver’s license can be presented for common branch services such as opening an account, reissuing a bankbook, applying for a debit card, changing a password, and updating customer information.

However, depending on the type of transaction and the bank’s internal policies, additional documents or another form of identity verification may be required.

Legal Basis for Driver’s License Identification

Recognition Under the Road Traffic Act

Article 85-2 of the Road Traffic Act provides that national institutions, local governments, public organizations, and businesses may use a physical or mobile driver’s license when they need to verify a person’s name, photograph, address, resident registration number, or other personal information for business purposes.

Priority of Other Applicable Laws

Banks may use a driver’s license to verify a customer’s identity because they are businesses that provide financial services.

However, if another law separately specifies an identification method for a particular transaction, the requirements under that law may take priority.

Identity Verification Under the Real-Name Financial Transaction Rules

Information Checked by Bank Employees

Banks must confirm a customer’s legal name and identity in accordance with laws governing real-name financial transactions.

A bank employee may check the name and resident registration number shown on the driver’s license and compare the photograph on the license with the person visiting the branch.

Electronic Verification and Additional Questions

When necessary, the bank may electronically verify the issuance information and validity of the identification document.

Presenting a driver’s license does not mean that every transaction will be completed without further questions. The customer may also be asked about the purpose of the transaction, the intended use of the account, or the source and intended use of the funds.

Banking Services Available With a Physical Driver’s License

Deposit Accounts and Card Services

A valid physical driver’s license can be used when opening a new checking or savings account, applying for a savings product, reissuing a bankbook, obtaining a debit card, or applying for a cash card.

Customer Information and Electronic Banking Services

A driver’s license may also be presented for identity verification when changing an account password, updating an address, or applying for internet banking.

Large Withdrawals and Transfer Limit Changes

A driver’s license can also be used when making a large withdrawal from an existing account or requesting a change to the transfer limit.

However, transactions with a higher risk of financial fraud may require additional verification, such as authentication through a mobile phone registered in the customer’s name, confirmation of the account password, review of recent transactions, or additional security questions.

Additional Requirements When Opening an Account

Verification of the Account’s Intended Purpose

A driver’s license allows you to apply for a new bank account, but presenting identification alone does not guarantee that every account will be opened immediately.

To prevent fraudulent accounts and voice-phishing crimes, banks may ask customers to explain why they need the account.

Documents for a Salary Account

When opening an account to receive salary payments, the bank may request an employment certificate, employment contract, or pay statement.

Documents showing the name of the employer and confirming that salary payments will be deposited may be required.

Documents for a Business Account

When opening an account for business purposes, the bank may request a business registration certificate, transaction agreement, tax invoice, or other documents showing actual business activity.

Limited-Transaction Accounts

If the supporting documents are insufficient or the purpose of the account cannot be adequately verified, the bank may initially open an account with restricted transfer and withdrawal limits.

Can You Use a Mobile Driver’s License at a Bank?

Using an Official Mobile Identification Document

An officially issued mobile driver’s license can be used for identity verification if the bank supports the relevant mobile identification service.

Difference Between a Photograph and an Official Mobile ID

A mobile driver’s license is not a photograph of a physical license taken with a smartphone camera.

It must be an official digital identification document issued through the government-approved Mobile ID app after the holder completes identity verification.

Identity Verification Without a Physical License

By opening the mobile driver’s license on a smartphone and completing the authentication procedure requested by the bank, a customer may verify their identity without presenting a physical driver’s license.

Mobile Driver’s License Verification at a Bank Branch

Requesting Mobile ID Verification

When using a mobile driver’s license at a bank branch, tell the bank employee that you would like to use a mobile identification document.

Scanning the QR Code

The employee may display a QR code on a branch terminal or tablet. The customer then opens the Mobile ID app and scans the QR code.

Consent to Information Sharing and Authentication

The customer reviews the identity information that will be provided to the bank, agrees to share the information, and completes the required authentication.

After authentication, the customer’s identity information is securely transmitted to the bank.

Authenticity Verification

The bank verifies the authenticity of the identification information through the mobile identification system.

Once verification is completed, the bank can proceed with the requested service, such as opening an account or updating customer information.

Mobile Verification Through a Banking App

Opening the Mobile ID App

When opening an account through a banking app, the customer may be able to select a mobile driver’s license as the identification method.

The banking app then connects to or opens the Mobile ID app to complete identity verification.

Returning to the Banking App

The customer completes authentication and consents to sharing personal information in the Mobile ID app.

Afterward, the customer returns to the banking app and continues the remaining application steps.

Additional Identity Verification

Depending on the bank, additional verification may be required through a mobile phone registered in the customer’s name, an existing bank account, facial recognition, comparison of the customer’s face with the identification photograph, or a video call.

Introduction of Mobile Driver’s Licenses at Banks

Launch of In-Branch Financial Services

According to information released by the Financial Services Commission, financial transactions using mobile driver’s licenses became available on July 28, 2022, at branches of 13 banks.

The participating institutions included KB Kookmin Bank, Shinhan Bank, Woori Bank, Hana Bank, NH NongHyup Bank, Suhyup Bank, Industrial Bank of Korea, and several regional banks.

Initial Use Through Banking Apps

At the time of the launch, non-face-to-face use was first offered through the apps of Shinhan Bank, Woori Bank, NH NongHyup Bank, and KakaoBank.

Expansion to Other Financial Institutions

Mobile identification systems were later expanded so that more banks and financial institutions could use official mobile identification documents.

Differences in Support Among Banks

Services Available at Bank Branches

Some banks allow customers to use a mobile driver’s license for services such as opening an account at a branch or updating customer information.

Services Available Through Banking Apps

Other banks may support mobile driver’s licenses only for certain transactions or only when opening an account through a banking app.

Differences Between Branches

Even within the same bank, the available method may differ depending on the type of transaction or whether the branch has the necessary equipment.

If you plan to visit a bank with only a mobile driver’s license, it is advisable to contact the bank’s customer service center or the specific branch in advance.

Photographs and Screenshots of a Driver’s License

Stored Photographs Are Not Accepted

A photograph of a driver’s license stored on a smartphone or a screenshot of the license cannot be used as an official identification document at a bank.

Reasons Photographs Are Restricted

A photograph does not allow the bank to confirm whether the identification document is currently valid.

It may also have been copied, altered, or transferred to another person.

Real-Time Verification Through the Official App

To use a mobile driver’s license, the customer must open the official Mobile ID app and complete real-time authentication.

Differences From Private Verification Services

Driver’s license verification services offered through mobile carriers or private apps may not have the same legal status or range of use as an official mobile driver’s license.

The institutions and banking services that accept these private verification services may also differ.

Validity Period and Damage to the License

Expired Renewal or Inspection Period

If the renewal or inspection period has passed, or if the validity of the physical driver’s license cannot be confirmed, the bank may request another identification document.

Damaged Text or Photograph

A driver’s license may not be accepted if it is severely damaged and the name, resident registration number, or photograph cannot be clearly identified.

Major Difference Between the Photograph and Current Appearance

If the photograph is outdated and the holder’s current appearance is significantly different, or if alteration or forgery is suspected, the bank may require additional identity verification.

Checking the License Before Visiting

Before visiting a bank, check the driver’s license renewal or inspection period and make sure that the printed information and photograph are clearly visible.

Loans and High-Value Financial Transactions

Identity Verification for Loan Applications

A driver’s license can be presented as an identification document when applying for a loan.

However, loan applications also involve an assessment of income, employment, creditworthiness, and repayment ability.

Large Withdrawals and Foreign Exchange Transactions

A driver’s license may also be used for services requiring enhanced verification, including large cash withdrawals, foreign exchange transactions, and applications for financial investment products.

Additional Financial Documents

The bank may request proof of income, an employment certificate, transaction agreements, tax documents, or business-related records.

These additional documents are not required because the driver’s license is unacceptable. They are required because the financial transaction involves a separate review or screening process.

Documents Required for Transactions by a Representative

Identification of the Representative

A representative cannot handle another person’s banking transaction by presenting only the representative’s driver’s license.

The representative must provide identification along with documents proving that they have the authority to act on behalf of the account holder.

Authorization Documents

Depending on the transaction, the bank may request a power of attorney, certificate of registered seal, certificate of personal signature, or family relationship certificate.

Accounts for Minors and Inheritance Matters

Banking transactions involving a minor’s account, inheritance, or guardianship may require additional documents proving the relationship between the account holder and the representative.

Corporate Account Transactions

Corporate account transactions may require a corporate registration certificate, business registration certificate, corporate seal certificate, power of attorney, and other documents confirming the authority of the company and its representative.

What to Check Before Visiting a Bank

Preparing a Physical Driver’s License

For most ordinary branch services, prepare a valid physical driver’s license.

Check that the name, resident registration number, and photograph are clearly visible.

Confirming Mobile ID Support

When planning to use a mobile driver’s license, confirm that the bank and the specific branch support mobile identification services.

Checking the Smartphone and App

Make sure the Mobile ID app is updated and that it opens and authenticates correctly.

Authentication may be interrupted if the smartphone battery is low or the internet connection is unstable.

Reissuing a Mobile License After Changing Phones

If you recently changed your mobile phone or need to have the mobile driver’s license reissued, complete the reissuance process before visiting the bank.

Asking About Transaction-Specific Documents

For services such as opening an account, applying for a loan, handling a transaction as a representative, managing a corporate account, or processing an inheritance matter, contact the bank in advance to confirm which additional documents are required.

Conclusion

A valid physical driver’s license can be used as an identification document for most banking services at a branch.

An official mobile driver’s license may also be used for opening accounts and other financial services if the bank supports the mobile identification system.

However, additional documents or identity verification may be required for loans, large transactions, representative transactions, corporate banking, and other services involving enhanced verification.

A photograph or screenshot of a driver’s license stored on a smartphone is not accepted as official identification. To use a driver’s license digitally, it must be issued and presented through the official Mobile ID app.

Frequently Asked Questions

Can I Visit a Bank With Only My Driver’s License?

Yes. A valid physical driver’s license can generally be used as an identification document for most ordinary banking services.

However, depending on the transaction, you may also need a bankbook, personal seal, mobile phone registered in your name, or additional supporting documents.

Can I Open a New Bank Account With a Driver’s License?

Yes. You can apply to open a new bank account using a driver’s license.

The bank may request an employment certificate, employment contract, business registration certificate, or transaction-related documents to confirm the purpose of the account.

If sufficient supporting documents are not provided, the bank may open an account with restricted transfer limits.

Can I Use a Mobile Driver’s License for Banking?

Yes, provided that the bank supports the mobile identification service.

At a branch, the customer may scan a QR code provided by the employee through the Mobile ID app and then complete information-sharing consent and identity authentication.

For non-face-to-face services, the banking app may connect directly to the Mobile ID app.

Can I Use a Photograph of My Driver’s License?

No. A photograph or screenshot of a driver’s license stored on a smartphone cannot be used as an official identification document at a bank.

The bank cannot reliably confirm the validity or authenticity of the identification document through a photograph or screenshot.

Can I Use an Expired Driver’s License at a Bank?

An expired driver’s license may not be accepted for identity verification.

The bank may also request another identification document or additional authentication if the license is severely damaged or if the photograph differs significantly from the holder’s current appearance.

Can I Use a Driver’s License When Applying for a Loan?

Yes. A driver’s license can be presented as an identification document when applying for a loan.

However, the bank will also assess income, employment status, creditworthiness, and repayment ability. Proof of income, employment certificates, and business-related documents may therefore be required.

Is a Driver’s License Enough to Handle Someone Else’s Banking Transaction?

No. A representative cannot complete another person’s banking transaction with only the representative’s driver’s license.

Documents such as a power of attorney, certificate of registered seal, certificate of personal signature, or family relationship certificate may also be required.

The exact requirements depend on the bank and the type of transaction.

Do All Banks Accept Mobile Driver’s Licenses?

The availability of mobile driver’s license verification and the services that can be completed with it may differ by bank.

Some banks may accept it at branches but not through their banking apps, while others may allow it only for selected financial services.

It is advisable to check with the bank before using a mobile driver’s license.